SAF : THE REAL CURRENCY FOR THE JETSET

Intro

The private jet has long symbolized ultimate freedom. Yet today, the real luxury in aviation isn’t speed or exclusivity—it’s simply having fuel that’s accessible. Sustainable Aviation Fuel (SAF)—the industry’s much‑touted alternative—still represents a slender 0.2% of global jet fuel consumption, projected to rise to just 0.7% by 2025. Meanwhile, SAF remains 4 to 5 times more expensive than conventional kerosene, largely due to regulatory fees and production constraints.

Compounding this scarcity, private aviation is witnessing a technology paradox: manufacturers are racing to design jets capable of flying entirely on SAF, equipped to land at remote or short-runway airports at the fastest time record—yet policies and limited fuel supply currently cap usage to blends of 50% or less, barring full SAF deployment until supply catches up.

For private jet operators, this isn’t environmental lip service—it’s a logistical and economic hurdle. The real challenge is no longer whether the aircraft can perform—it’s whether the right fuel is available at the right place and time.

In a sector built on seamless travel and ultimate flexibility, the scarcity and cost of SAF introduce a new dimension to luxury: fuel access itself has become part of the experience equation.

What is SAF, in Simple Terms?

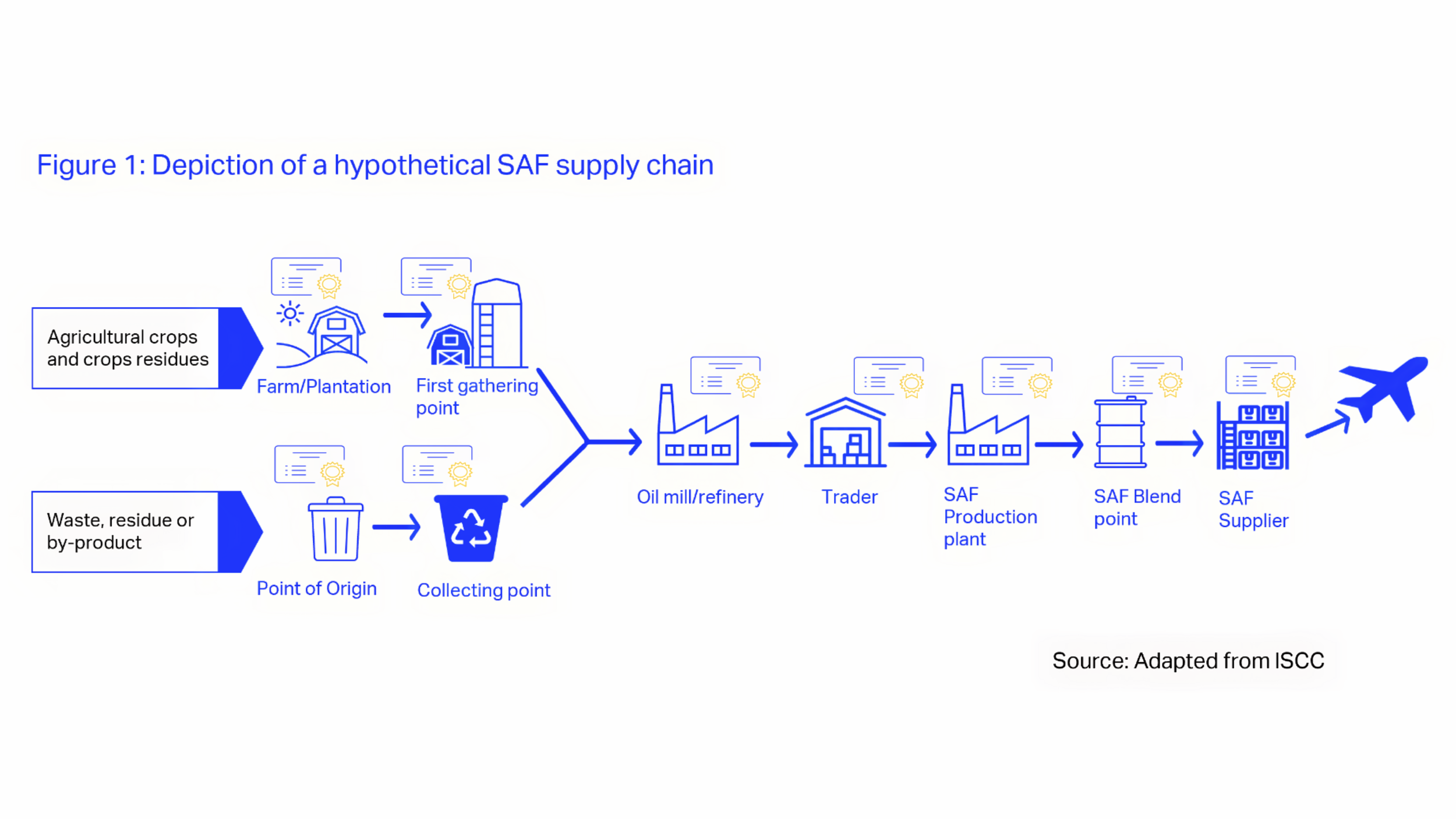

Sustainable Aviation Fuel (SAF) is jet fuel made from non-petroleum feedstocks—like waste cooking oil, plant residues, municipal waste, and even algae.

It has been in development for over a decade, with one of the earliest experimental flights in 2008 when Virgin Atlantic used a blend derived from coconut and babassu oils.

Fast forward to November 2023, an industry consortium led by Virgin Atlantic successfully flew the first fully 100% SAF-powered transatlantic commercial flight—demonstrating the technical feasibility of long-haul travel on SAF.

Drop-in Fuel & Blending Constraints

Technologically, SAF is a “drop-in fuel,” meaning it blends seamlessly with conventional kerosene and works in today’s aircraft—and within the existing fueling infrastructure. However, current regulations limit SAF blending to a maximum of 50%, even though engines can technically handle 100% SAF. This restriction exists because of supply constraints—not technical limitations.

Commercial Aviation vs. Private Aviation Access

Although global SAF supply is projected to reach just 0.7% of aviation fuel by 2025, according to IATA projections reported by Reuters, commercial airline operators—who face mounting regulatory mandates such as the EU’s ReFuelEU (requiring SAF blending from 2% in 2025 up to 70% by 2050)—are naturally prioritized in allocation.

This institutional weight and volume purchasing give them priority access to SAF, leaving private aviation, technically fully capable, with inconsistent access and higher costs.

A Paris–Nice hop (~1 hr flight, ~1,200 L fuel) could incur a €3,000–€4,000 premium if fueled by SAF—affordable to clients but unsustainable for operators running multiple daily flights.

A London–New York trip (~7 hr, ~18,000 L fuel) could see the SAF premium balloon to €40,000–€50,000 per flight, significantly stressing profitability or client expectations.

NetJets: Bridging the Gap

Among private operators, NetJets has emerged as a clear leader in addressing SAF scarcity:

In 2024, it purchased 19.4 million gallons of SAF, doubling its prior year and cementing its position as the largest SAF buyer in private aviation.

It secured supply pipelines through strategic agreements with Signature Flight Support and Neste, ensuring SAF availability at hubs such as San Francisco and London–Luton.

NetJets also committed to buying 100 million gallons over 10 years from WasteFuel, a bold move designed to guarantee future access while supporting scaling of production.

In context, the 19.4 million gallons used in 2024 represents a substantial share of the operator’s overall fuel needs, reflecting a deliberate strategic pivot toward long-term SAF adoption—even if the precise proportion remains proprietary.

This type of foresight differentiates NetJets during a critical phase of luxury aviation’s evolution: in a market where fuel access is becoming the rarest commodity, securing supply today means securing relevance tomorrow.

Focus: Technical Limits vs. Policy Mandates

It is important to distinguish between technical certification limits and policy blending mandates.

1. The 50% Blending Limit (Technical Certification Rule)

Today, under ASTM D7566 certification, aircraft are only approved to fly with up to 50% SAF blended with conventional kerosene.

This is a safety and certification limit, not a market mandate.

Even though engines are technically capable of flying on 100% SAF, global certification rules haven’t yet been updated for full adoption.

Source: Air Transport Action Group (ATAG) & IATA fact sheets.

2. EU ReFuelEU Mandate (Policy Requirement)

The ReFuelEU Aviation regulation sets minimum SAF usage targets for all fuel supplied at EU airports.

These are policy blending requirements, not technical limits.

Targets: 2% in 2025, 6% in 2030, 20% in 2035, and 70% by 2050.

This means fuel providers must ensure that a certain share of available jet fuel is SAF—within the existing 50% technical blending cap.

Why Demand is Rising

So why pursue SAF despite its high cost? The pressure is coming from three converging fronts. Regulation is tightening, with the EU mandating a 6% SAF blend by 2030 and higher targets beyond, mirrored by the UK and several Asia-Pacific states—standards that private jets cannot ignore. Client perception is shifting as corporations and ultra-high-net-worth individuals increasingly avoid association with what critics call “dirty luxury,” making SAF not only fuel but a reputational shield and brand differentiator. And in emerging markets, Asia’s SAF production ambitions are set to exceed local demand, creating new export opportunities, while the Middle East is both opening its skies to operators like VistaJet and investing heavily in biofuel research—evidence that access to SAF is becoming a defining factor in global aviation competitiveness.

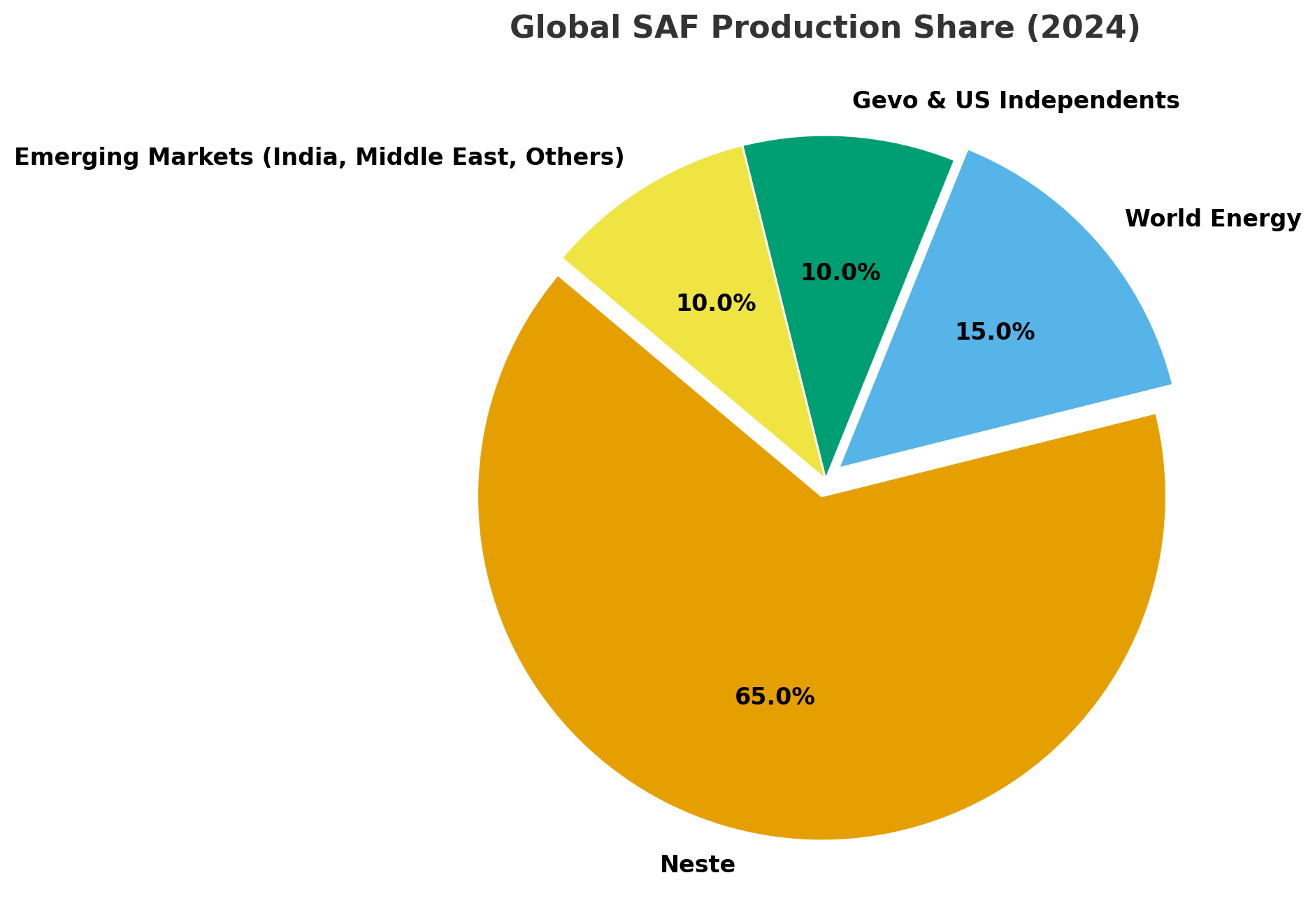

SAF Leaders

Behind the headlines on scarcity and cost, a handful of companies are quietly building the backbone of the SAF industry. Each is betting on different feedstocks, technologies, and geographies—but together they are shaping the contours of supply for the next two decades.

Neste (Finland): The undisputed market leader and currently the world’s largest SAF producer, Neste operates refineries in Europe, Asia, and the United States. The company is scaling to produce over 1.5 million tonnes of SAF annually by 2026, leveraging a global logistics network that already supplies both commercial airlines and business aviation operators.

SkyNRG (Netherlands): One of the earliest pioneers in SAF, SkyNRG is backed by KLM and Shell and has built a reputation around scalable, long-term projects. Its DSL-01 facility, due to open in 2026, will be Europe’s first dedicated SAF plant, producing 100,000 tonnes per year. SkyNRG has also been a driving force in developing “book-and-claim” models, allowing airlines and private operators to purchase SAF credits even where infrastructure is lacking.

IndianOil (India): In Asia, IndianOil has become the flagbearer for large-scale SAF production. It was recently certified to produce SAF from used cooking oil, with a target of 35,000 tonnes annually. Positioned in one of the world’s fastest-growing aviation markets, IndianOil’s production is expected to support both domestic demand and potential export opportunities to Europe and the Middle East.

Gevo (USA): A Colorado-based company specializing in alcohol-to-jet (ATJ) technology, Gevo has signed long-term offtake agreements with airlines including Delta and American. Its Net-Zero 1 plant, expected to be operational by 2025, aims to deliver 45 million gallons per year of SAF. Gevo’s strategy hinges on integrating renewable energy into its production, positioning itself as a “circular economy” fuel supplier.

World Energy (USA): Founded in 1998 in Boston, Masssachusetts. One of the first commerical-scale producers of renewable fuels. Its SAF role comprises of operating the Paramount refinery in California, one of the world´s first facilities to produce SAF at scale. Supplies SAF to major airlines including United, JetBlue, and DHL, and works closely with OEMs and energy companies such as Honeywell, Gulfstream for certification testing.

ADNOC (UAE): Partnering with Boeing and Masdar on SAF development, with a focus on synthetic fuels and carbon capture integration. Seen as a key regional player for scaling supply in the Gulf.

Emirates (UAE): Conducted one of the first 100% SAF demonstration flights in 2023 using a Boeing 777. While not a producer, Emirates’ public investment in SAF signals strong demand pull and policy influence in the region.

Saudi Aramco (Saudi Arabia): Exploring large-scale biofuel production through joint ventures with TotalEnergies and local research centers, aiming to leverage Saudi Arabia’s refining infrastructure for SAF export.

Together, these companies highlight the diverse approaches shaping SAF: Neste’s global scale, SkyNRG’s pioneering partnerships, IndianOil’s emerging market momentum, and Gevo’s technology-driven model. For private aviation, keeping close to these leaders—through partnerships, credits, or direct offtake agreements—may be the only way to guarantee access in a constrained market.

Market Overview

~1.3 billion liters (~1 million tonnes), covering ~0.3% of aviation fuel demand. Projection by 2030: 8–10% of global jet fuel demand, depending on policy incentives and feedstock availability (IATA).

Stakeholders’ Strategies to Solve the Problem

Because SAF cannot scale overnight, the industry is experimenting with workarounds:

Book & Claim : Passengers or operators pay for SAF use “virtually,” even if the airport doesn’t have SAF infrastructure. This helps signal demand while scaling production.

Partnerships & Investments: Jet operators co-investing in SAF projects with energy companies to secure supply.

Policy Support: Governments are offering subsidies, tax credits, and mandates to accelerate SAF capacity. For example, the US Inflation Reduction Act includes major SAF incentives.

But uncertainty remains. According to BCG, without stronger demand signals and long-term contracts, SAF may struggle to hit the volumes needed before 2030.

The Strategic Outlook

Short-term (2025–2030): SAF remains scarce, costly, and mostly symbolic for private aviation. Adoption will be concentrated among operators marketing themselves as sustainability leaders.

Medium-term (2030–2040): Production expansion in Asia, the US, and the Middle East could ease supply constraints, though costs will remain higher than fossil fuels.

Long-term: For private aviation, SAF is less about cost and more about relevance. In an era of climate scrutiny, access to SAF may determine which operators remain attractive to high-profile, sustainability-conscious clients.

Closing

In luxury aviation, fuel is no longer just fuel—it’s a statement. SAF is scarce, expensive, and complex—but it’s also the only runway toward a future where private aviation remains both aspirational and acceptable.

References:

Air Transport Action Group (ATAG). (n.d.). Sustainable aviation fuel. https://atag.org/industry-topics/sustainable-aviation-fuel

Aviation International News (AIN Online). (2020, September 23). VistaJet signs SAF use agreement. https://www.ainonline.com/aviation-news/business-aviation/2020-09-23/vistajet-signs-saf-use-agreement

Chooose. (2024). Benefits and considerations of sustainable aviation fuel. https://www.chooose.today/resources/learning-resources/benefits-and-considerations-of-sustainable-aviation-fuel

GreenAir News. (2021, January 21). Neste and NetJets establish strategic partnership to advance sustainable aviation fuel in business aviation. https://www.greenairnews.com/?p=1881

GreenAir News. (2025, January 9). IATA estimates the industry will spend $281 billion on fuel this year. https://www.greenairnews.com/?p=5103#:~:text=IATA%20estimates%20the%20industry%20will,industry%20fuel%20bill%20this%20year

International Air Transport Association (IATA). (n.d.). Fact sheet: Sustainable aviation fuels. https://www.iata.org/en/iata-repository/pressroom/fact-sheets/fact-sheet-sustainable-aviation-fuels/

International Air Transport Association (IATA). (2024, December 10). IATA: SAF production to double in 2025 to 1.9 million tonnes. https://www.iata.org/en/pressroom/2024-releases/2024-12-10-03

International Energy Agency (IEA). (n.d.). Aviation. https://www.iea.org/energy-system/transport/aviation

NetJets. (2023). NetJets expands global sustainability program. https://www.netjets.com/en-us/expanded-global-sustainability-program

Reuters. (2025, January 9). Idemitsu to begin trial of non-edible oilseed crop aviation fuel. https://www.reuters.com/markets/commodities/idemitsu-begin-trial-non-edible-oilseed-crop-aviation-fuel-2025-01-09/

Rocky Mountain Institute (RMI). (2024, March 6). Unraveling willingness to pay for sustainable aviation fuel. https://rmi.org/unraveling-willingness-to-pay-for-sustainable-aviation-fuel/

Signature Aviation. (2020, September 23). Neste and NetJets establish strategic partnership. https://www.signatureaviation.com/news/neste-and-netjets-establish-strategic-partnership

Simple Flying. (2024, February 9). NetJets purchases 20 million gallons of SAF in 2024. https://simpleflying.com/netjets-purchases-20-million-gallons-saf-2024

S&P Global Commodity Insights. (2025, June 2). Airlines see relief with 86% jet fuel SAF costs hinder sustainability: IATA chief. https://www.spglobal.com/commodity-insights/en/news-research/latest-news/agriculture/060225-airlines-see-relief-with-86-jet-fuel-saf-costs-hinder-sustainability-iata-chief

Virgin Atlantic. (2023, November 28). World’s first 100% sustainable aviation fuel flight across the Atlantic. https://corporate.virginatlantic.com/gb/en/media/press-releases/worlds-first-sustainable-aviation-fuel-flight.html

VistaJet. (2020). VistaJet signs SAF use agreement. https://www.ainonline.com/aviation-news/business-aviation/2020-09-23/vistajet-signs-saf-use-agreement

World Energy. (2024). SAF policy around the world. https://worldenergy.net/resource/saf-policy-around-the-world

ESG Today. (2025, January 5). Global sustainable aviation fuel production to double in 2025, IATA says. https://www.esgtoday.com/global-sustainable-aviation-fuel-production-to-double-in-2025-iata-says

International Transport Forum (ITF). (2021). Sustainable aviation fuels policy status report. https://www.itf-oecd.org/sites/default/files/docs/sustainable-aviation-fuels-policy-status-report.pdf